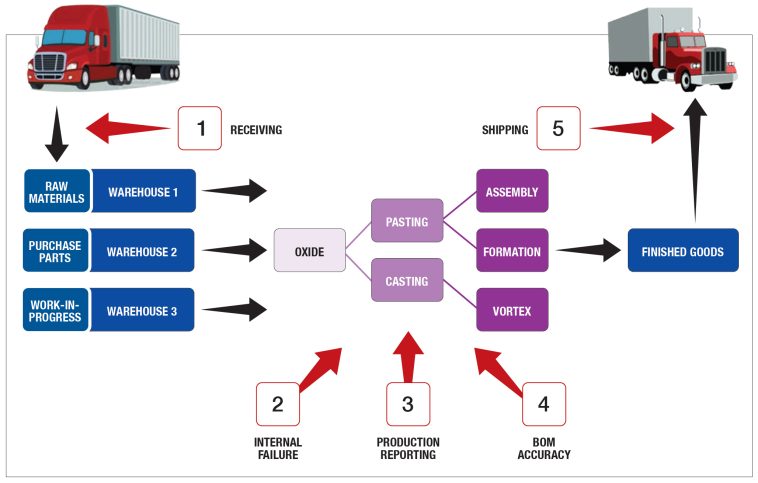

The Five Gateways of Inventory Control: A Manufacturing Perspective

Inventory management is the backbone of many industrial manufacturers, especially when the products in question are as critical as automotive batteries or electric vehicle components. Over the years, firms have learned that the hidden complexities of production—those tricky parts of raw material handling, reporting, and shipping—are best tackled with systematic controls. In this opinion editorial, I share insights and personal perspectives on how robust internal controls can make a significant difference in financial reporting, process efficiency, and overall business performance.

By looking at a well-documented case study from a historical facility, we can understand how companies have succeeded—and sometimes struggled—while managing the five essential gateways of inventory control.

Essential Material Handling: Raw Materials and Purchase Parts Receipt

One of the first and most critical checkpoints in inventory management is the reception of raw materials and purchased parts. In manufacturing environments, the potential for loss or misstatement is high if inventory receipts are not carefully monitored. Even a small discrepancy from the agreed purchase order can translate into significant cumulative losses over time.

Preventing Overstatements and Losses

At the receiving dock, the daily challenge is to ensure that the quantity recorded in the system accurately reflects the physical material delivered. For example, when dealing with large-scale deliveries—such as 30 truckloads of lead or specialized batteries—the temptation is to assume that the goods arriving are exactly as documented on the paper trail. However, the process involves many twists and turns that can lead to tangled issues, such as overstatements in goods received.

A routine approach to preventing these issues includes the use of:

- Daily cycle counts and physical verifications

- Weighing procedures for bulk materials

- ERP system cross-checks with physical data

- Detailed inspection protocols at the dock

These measures help ascertain that the physical properties—such as weight in the case of lead hogs—match what is entered into the software. Failure to do so might generate minor differences that, in cumulative financial terms, are far from negligible.

Integrating Technology With Manual Oversight

In this age of digital solutions, smart tools like radio frequency identification (RFID) scanners play a key role, allowing companies to use technology to get around complicated pieces of manual entry work. However, manual oversight remains crucial: a human eye in the loop helps ensure that digital entries adhere to realistic expectations, and any dissonance can be quickly rectified.

| Key Step | Potential Pitfall | Control Mechanism |

|---|---|---|

| Receiving and Verification | Overstated quantities | Physical weighing and match with ERP |

| Documentation | Data entry errors | Cycle counts and supervisory checks |

This table summarizes how integrating daily checks with automated systems reduces the risk of inventory discrepancies.

Controlling Internal Failures: Tackling Scrap and Nonconforming Products

The second gateway addresses the challenges of internal failure. In the manufacturing world, scrap—that is, defective or nonconforming product—is an unavoidable outcome of production processes. However, while some level of scrap is normal, unmonitored losses can be both overwhelming and detrimental to the financial health of the company.

Understanding Scrap as a Byproduct of Process Variation

Every production process will yield some waste. The key is to sort out when the waste is within acceptable limits and when it starts to represent a larger problem. The everyday task involves tracking scrap meticulously and assigning it the correct accounting treatment. Failing to do so may result in scrap dollars staying on the balance sheet when they rightly belong in the cost of goods sold.

Quality management techniques, such as the principles of Six Sigma or statistical process control (SPC), help companies reduce these tangled issues. These approaches emphasize:

- Continuous improvement and lean manufacturing techniques

- Routine inspections and quality assurance checks

- The use of key performance indicators to monitor output

- Regular audits to verify the accuracy of scrap reporting

In many instances, the challenges are not just about controlling the scrap, but also addressing when scrap is misclassified in the financial records, thus affecting the inventory valuation.

Aligning Financial Controls With Operational Realities

The ability to catch discrepancies quickly is super important in inventory control. In practice, companies establish systems that trigger immediate write-downs and reclassifications when scrap is identified. By doing this, they ensure that losses are recorded in the right place, allowing for accurate financial reporting at month-end or year-end. Additionally, this process facilitates a smoother interaction with external auditors, who often focus on these internal failure rates during their assessments.

When internal failures are regularly monitored and reported, companies can also leverage the resulting data to refine their forecasting models and make informed decisions about production scheduling, raw material ordering, and overall process improvements.

Production Reporting Realities: Keeping Track of Work-in-Progress

The third gateway centers around production reporting. In manufacturing, work-in-progress (WIP) stages are where the assembly line creates the next level of the finished product. This process can become loaded with tricky bits—especially when production figures are overstated to meet short-term corporate objectives.

Ensuring Accuracy in a Fast-Paced Environment

The production stage often involves a fast flow of operations, where quantities are recorded using systems integrated with bar-code scanning and RFID detection. A common predicament is when numbers reported by the production teams are slightly off, either due to rushed data entry or misalignment between physical production and recorded activity. Such deviations, while they may seem small, can add up to significant variances at the end of a reporting period.

To address these issues, manufacturers implement:

- Continuous cycle counting throughout production facilities

- Independent audits by materials managers

- Real-time reconciliation between physical movement and recorded data

- Clear communication channels between production teams and financial control staff

This process ensures production tallies match the physical reality, reducing the likelihood that excessive inventory appears in the financial statements. At the same time, it bolsters confidence among external auditors and internal stakeholders.

Innovative Approaches to Capture Production Data

Several modern manufacturing firms have taken the step to segregate production reporting from cycle counting. For instance, while the production team handles the day-to-day records, a dedicated group of cycle counters operates independently. Their role is to walk the production floor, occasionally get into the nitty-gritty details, and verify that each pallet’s barcode, quantity, and storage location are accurately captured in the system.

This separation of duties is critical. It helps avoid a situation where misreported figures by the production team are simply perpetuated in the system without an external check. Such an approach not only improves inventory accuracy but also mitigates the risk of internal control failures being flagged during an audit.

Bill of Material Accuracy: Straightening Out the Fine Points

The fourth gateway, the accuracy of the bill of materials (BOM), is perhaps one of the most overlooked—even yet one of the most key—elements in inventory control. The BOM dictates the precise mix of raw materials, components, and subassemblies necessary to build the final product.

Bridging the Gap Between ERP Data and Physical Reality

Typically, the assumption is that if the ERP software contains a BOM, it must be correct. However, many issues arise from the confusing bits where the ERP data and the on-the-floor usage diverge. For example, quality assurance might allow for a slight variation in materials used per unit, which, when scaled to thousands of units, may represent a measurable gain or loss in inventory.

Consider these aspects when tackling BOM accuracy:

- Regular verification of BOM data with actual production records

- Implementation of change management processes for engineering alterations (ECOs)

- Frequent cross-checks between the production, quality assurance, and accounting departments

- Detailed analysis of the cost per unit variation

In practice, engineering change orders (ECOs) play a significant role. They can lead to material gains and losses that need to be accounted for as soon as the updates are implemented. If a newer mold or process reduces the use of material slightly, companies must promptly adjust the BOM to reflect this subtle shift; otherwise, the resulting differences might manifest as significant financial variances.

Combining Technology With Managerial Acumen

Modern manufacturing facilities use sophisticated ERP systems to maintain their BOM records. Nonetheless, technology alone is not enough to capture all the little twists that occur in practice. It is essential for accounting professionals to work closely with production and engineering teams to get into the fine details—not just relying on automated data feeds, but rather reviewing periodic reports and undertaking random checks.

To further illustrate, here is a simple table outlining potential scenarios that can arise from BOM discrepancies:

| Scenario | Potential Impact | Control Recommendation |

|---|---|---|

| Material Overuse in Production | Inventory loss affecting cost of goods sold | Regular audit and recalibration of BOM standards |

| Use of Substituted Components | Unexpected cost differentials | Real-time verification of component usage |

| Engineering Updates to BOM | Perceived material gains or waste | Clear communication protocol and immediate adjustment in ERP |

This approach underscores the need for constant vigilance. Only by aligning ERP data with the physical counts and engineering reality can companies ensure that their production costs remain true to the actual circumstances on the shop floor.

Shipping Verification: Final Checks That Cement Financial Integrity

The final gateway in inventory control is shipping verification. This stage marks the transition of items from inventory to cost of goods sold. Accurately tracking this phase is super important, as it directly affects not just inventory figures but also revenue recognition and overall financial reporting.

Ensuring the Right Transfer of Ownership

In practice, shipping is a highly structured process involving multiple verification points. As products leave the warehouse, material handlers pick the goods from their designated bins, assemble shipments, and scan the corresponding bar-code labels. Each of these steps is designed to ensure that the recorded transaction accurately reflects the physical movement of inventory.

What makes this process challenging is the possibility of miscommunication between systems and physical handling. For example, if a shipment is “ship confirmed” in the ERP system but a seal is broken or a pallet goes missing, the discrepancy must be detected as early as possible to avoid substantial financial write-downs.

Key control measures at the shipping verification stage include:

- End-of-shift audits for shipment accuracy

- Final checks performed by an independent security or guardhouse team

- Reconciliation between physical shipments and ERP confirmations

- Clear guidelines about the exact moment ownership transfers from the company to the customer

External auditors often emphasize this gateway since revenue recognition rules and cost of goods sold calculations depend heavily on timely and accurate shipping data. If shipments are recorded inaccurately, revenue might be recognized too early or too late, leading to a snowball effect on financial reporting.

Detailed Processes and Best Practices

Many organizations have found that incorporating a multi-step check at the docks can help mitigate these overwhelming challenges. Best practices include sealing shipments with a known tag, having a security guard verify the seal’s integrity, and confirming that the shipped goods register correctly in the system. In some cases, companies even use digital logs to capture real-time data about the movement of goods from inside the warehouse to the shipping area.

These checks serve as the final safety net, reinforcing the idea that effective inventory control is not a one-time setup but an ongoing process that requires diligent oversight at every step.

The Annual Physical Inventory: The Umbrella That Covers All Internal Controls

All the individual gateways—from raw materials reception to shipping verification—culminate in the annual physical inventory count. This process is super important because it serves as the final, independent check to ensure that all internal controls are functioning as designed. Whether you are dealing with overstatements from the dock or understated production figures, the annual count validates if the perpetual system is accurately reflecting the physical inventory.

Why the Year-End Inventory Count Matters

Conducting an annual physical inventory not only reassures stakeholders about the company’s financial transparency but also sets the stage for identifying any discrepancies. External auditors, as well as internal teams, pay close attention to any variations found during this period. A well-planned and executed inventory count is critical for:

- Validating documented financial statements

- Ensuring that cycle counting, scrap reporting, and production reporting are accurate

- Highlighting areas for operational improvement

- Identifying any recurring tangled issues in the processes

For some companies, especially those that elect a year-end during a slow sales period, this final check helps streamline the closing process. By aligning physical counts with their fiscal years, companies can reduce the chance for mistakes in their reported inventories.

Integrating the Count With Internal and External Audits

One of the best aspects of an annual inventory count is that it involves oversight from both internal and external audit functions. In many cases, representatives from the external audit team attend the count, ask detailed questions, and even conduct test counts. Such interaction confirms that all five gateways are effectively controlled and that any variances fall within acceptable thresholds.

A strong cycle counting protocol, combined with a rigorous annual physical inventory, sends a clear message: the company is serious about maintaining robust internal controls and accurate financial reporting. This kind of transparency not only benefits the company but also boosts shareholder confidence and aligns with compliance requirements such as those outlined in SOX Section 404.

Continuous Improvement and Ethical Leadership in Inventory Control

Beyond the mechanical workings of inventory checks, the role of robust internal controls lies in their ability to spur continuous process improvement and foster ethical leadership on the shop floor. Management accountants and controllers often find themselves stepping up as leaders who must steer through both operational inefficiencies and financial misstatements.

The Role of Management Accountants

Management accountants are uniquely positioned to get into the fine details of operational performance and financial reporting. They are tasked with:

- Working with both production and engineering teams

- Communicating subtle differences between recorded data and physical counts

- Identifying the root causes when variances exceed predetermined thresholds

- Ensuring that policies and procedures are clearly followed on a daily basis

These professionals must be comfortable engaging with the operational side of the business—a process that can often feel overwhelming due to the nerve-racking pace of production floors. Their daily “Gemba walks” (a term adopted from Japanese management philosophy) allow them to experience firsthand the real challenges faced by workers. In doing so, they can better advise on improvements and ensure that checks are implemented in ways that are both practical and effective.

Building a Culture of Accountability and Open Communication

Beyond the numbers, the success of inventory control hinges on a strong culture of accountability. Companies benefit from policies that empower employees to speak up if they notice issues or deviations from standard work instructions. In some organizations, measures such as third-party fraud hotlines or internal reporting channels have been introduced to ensure that issues are promptly addressed.

As companies evolve in response to ever-changing compliance requirements, ethical leadership remains a must-have quality among those in charge of financial oversight. Leaders must not only be technically adept but also able to foster a culture where questions are welcomed and solutions are collaboratively developed. This kind of leadership ensures that any discrepancies are not swept under the rug but are instead seen as opportunities to refine processes and strengthen overall controls.

Lessons Learned From a Case Study: Exide Technologies’ Experience

The experience of Exide Technologies’ plant in Bristol, Tennessee, offers a prime example of how these five gateways can be implemented successfully—and where lapses may occur. In that facility, the plant manager, production manager, controller, and materials manager had well-defined roles that collectively ensured that inventory was controlled meticulously.

The Impact of SOX Section 404 Compliance

SOX Section 404: Management Assessment of Internal Control radically changed how companies approach their internal processes. At Exide, the introduction of a demanding checklist—the Exide Internal Control Environment (EICE) checklist—required quarterly reviews of asset-related processes, most notably those involving inventory and fixed assets. Although this added a layer of complexity, it also forced the creation and maintenance of clear, documented procedures aimed at reducing deviations.

This regulatory change underscored a few key points:

- Strong internal controls are not optional but essential for reliable financial reporting.

- Regular review of controls via internal audits and cycle counts is key to detecting and correcting errors.

- Close collaboration with external auditors ensures that inventory variances are taken seriously and addressed in a timely manner.

Exide’s case illustrates that while implementing such a system may seem intimidating at first, the eventual outcome is an enhanced level of accountability and increased accuracy in financial reporting.

Incorporating Best Practices Across All Gateways

Over the years, Exide and similar organizations have adopted best practices that can be summarized as follows:

- Maintain up-to-date written policies and procedures for each inventory control gateway.

- Use technology in tandem with hands-on oversight to monitor inventory changes.

- Regularly review data from cycle counts, production reports, and BOM updates to spot discrepancies early.

- Establish a clear chain of command so that any concerns raised at the shop floor level are quickly escalated and resolved.

- Leverage external audit insights to continuously improve internal control measures.

These practices not only ensure that variances are minimized but also help create a proactive environment where all levels of management are vigilant and accountable. The lessons learned from Exide’s experience remain relevant regardless of how technology evolves or how market conditions shift.

Conclusion: A Blueprint for Robust Inventory Control

In today’s dynamic manufacturing and industrial landscape, establishing robust inventory control is more than a regulatory requirement—it is a crucial element of sound business strategy. The five gateways of inventory control serve as a comprehensive framework that covers everything from the receipt of raw materials to the final shipping verification. By addressing each gateway with dedicated oversight and integrating technology with human expertise, companies can effectively manage inventory, reduce losses, and enhance financial reporting accuracy.

Whether you are an operations manager, a financial controller, or an external auditor, these processes offer a roadmap for reducing the overwhelming risks associated with inventory mismanagement. They allow businesses to steer through the maze of production reporting, BOM accuracy, and internal failure control with confidence—a pathway that ultimately leads to reliable financial statements and sustainable growth.

It is crucial that companies remain adaptable, continuously reviewing and refining their processes to keep up with evolving market demands and compliance standards. With ethical leadership, open communication, and an unwavering commitment to accuracy, manufacturing firms can overcome the challenging bits of internal control and position themselves well for the future.

Employing best practices, such as those highlighted from Exide Technologies’ experience, provides a blueprint for success—not only from a compliance standpoint but also as a means to drive operational improvements and strategic decision-making. As these companies evolve and innovate, their underlying controls must do the same, ensuring that every subtle detail contributes to a transparent, efficient, and financially sound organization.

Ultimately, the journey through these five gateways is not just about ticking boxes on an audit checklist. It is about embedding a culture of meticulous attention to detail and proactive problem-solving at all levels of the organization. For professionals with a stake in manufacturing, committing to these practices is not only smart accounting—it is sound business.

In closing, the insights gleaned from the case study underscore a simple, yet powerful message: a well-governed inventory control system protects the company’s assets, reveals improvement opportunities, and inspires confidence among investors, auditors, and employees alike. As we look ahead to an increasingly competitive industrial landscape, the ability to effectively manage inventory and maintain robust internal controls will remain a key differentiator for successful companies.

By staying engaged with processes from raw material receipt through to shipping verification—and by ensuring that every internal control gateway is clearly defined and vigilantly monitored—manufacturers can overcome the nerve-racking challenges of operational variability. With clear policies, cross-functional teamwork, and modern technology in place, firms can confidently face whatever twists and turns the business environment presents.

Originally Post From https://www.cpajournal.com/2025/07/16/the-five-gateways-of-inventory-control-2/

Read more about this topic at

Mastering Inventory Logistics: Key Strategies for Supply Chains

Mastering Inventory Control: Methods and Systems